Zero per cent financing might sound like a great deal - no interest charges, lower overall costs, and the ability to spread payments over time. But these offers often come with strict conditions and trade-offs, like requiring a high credit score (700+), limiting eligible vehicles, and forcing you to give up cash rebates or negotiate less on the vehicle price.

Here’s what you need to know before applying:

- Eligibility: Typically requires a credit score of 700 or higher.

- Vehicle Limitations: Only available on specific models or trims, usually new cars.

- Hidden Costs: You may lose out on cash rebates or face higher sticker prices.

- Shorter Terms: Often limited to 24–48 months, leading to higher monthly payments.

Before committing, compare the total costs of a 0% offer with a traditional loan that includes rebates. Sometimes, paying a small interest rate on a lower loan amount can save more money overall. Always negotiate the car price first and ensure the deal fits your budget.

The TRUTH About 0% Car Loans

sbb-itb-20f5d75

Common Misconceptions About 0% Financing

A lot of Canadian car buyers believe 0% financing is a blanket offer available for any vehicle they choose. However, these promotions come with strict conditions that can trip you up if you’re not paying attention to the fine print. Knowing these common misconceptions can help you decide if a 0% financing deal works for your budget.

Limited to Specific Models and Trims

0% financing isn’t available across the board - it’s typically limited to certain models. Automakers often use these deals to boost sales of slower-moving vehicles or those with higher profit margins. For instance, in February 2026, Chevrolet offered 0% financing for 60 months on the 2026 Silverado 1500 and the 2025 Corvette Z06, but excluded other models from the same terms. Similarly, Cadillac restricted its 84-month 0% financing offer to the 2026 CT4 and CT5, while the 2025 XT5 and XT6 were capped at 60-month terms.

Another catch is that these offers often apply to models with added options, pushing their price above the base MSRP. For example, in April 2025, Nissan’s 0% financing for up to 60 months was only available on the 2025 Rogue SL trim - not the base model. And don’t expect to find 0% deals on used cars - these promotions are almost always reserved for new vehicles.

Requires Excellent Credit to Qualify

Even if you find a qualifying vehicle, you’ll need an excellent credit score to secure 0% financing. Lenders take on more risk with these loans since they don’t earn interest, so they reserve them for buyers with top-tier credit. Generally, you’ll need a credit score of at least 700, but some automakers set the bar higher, requiring scores of 725 or even 760 for approval.

To put this into perspective, in Q1 2025, even "Super prime" borrowers with scores of 781+ paid an average interest rate of 5.18% on new car loans. That makes 0% financing a rare and exclusive opportunity for those with near-perfect credit.

"0% financing is when the dealership lets you finance a car and, instead of charging interest, they let you pay it off with zero interest... these deals are usually for folks with tip‑top credit scores." - Clutch

Vehicle Prices May Be Higher

Opting for 0% financing often means sacrificing manufacturer cash rebates, which can range from $3,000 to $6,000. Additionally, dealerships are less likely to negotiate the vehicle’s price when a 0% deal is in play. While it may seem like you’re avoiding interest costs, those costs are often hidden in the rebate you didn’t get.

"The truth is, the dealer already added the interest into the price of the car and disguised it as a 'rebate.' That $4,500 'discount' is really just the interest cost baked into the financing deal." - Truth Concepts

"Auto manufacturers will often choose the most profitable models to offer 0% interest on... these 0% financing models are often loaded with profit‑building options and packages that drive pricing well above the base MSRP." - Clutch

Before committing, compare the overall cost of a 0% loan to a traditional loan that includes a cash rebate. In some cases, paying interest on a smaller loan amount can actually save you money compared to a 0% financing deal. These considerations highlight the importance of doing the math before signing on the dotted line.

What to Consider Before Applying

Signing up for a 0% financing deal might seem like a no-brainer, but it's important to dig deeper before committing. While the idea of paying no interest is appealing, these offers can sometimes create financial challenges you might not expect. Factors like shorter repayment terms, restrictions on rebates, and hidden price adjustments can all impact your budget.

Shorter Terms Mean Higher Monthly Payments

One of the key trade-offs with 0% financing is the shorter repayment period. Unlike traditional car loans that can stretch out over 60, 72, or even 84 months, these interest-free offers typically cap repayment at 24, 36, or 48 months. The shorter timeline means higher monthly payments, even though you're not paying interest.

For instance, financing a $30,000 car at 0% over 36 months would result in monthly payments of $900. That's a hefty amount to budget for each month, so you'll need to carefully evaluate whether these payments fit comfortably within your financial plan.

Cannot Combine with Other Rebates or Promotions

Another limitation of 0% financing is that it usually doesn't allow you to combine the deal with cash rebates or other promotions.

"Stripping the rebate alone is sometimes enough to make up for the lack of interest charges." - Clutch

In many cases, opting for a traditional loan with a cash rebate might save you more money overall. It’s worth running the numbers to see which option truly offers the better deal, especially if the rebate is significant.

Hidden Costs in the Sticker Price

On the surface, a 0% deal might look like a win, but dealerships often find ways to make up for the lost interest income. This can include inflating the sticker price, tacking on administrative fees, or reducing your ability to negotiate.

"You're not getting a discount on the car - you're just paying interest in disguise." - CarRefinancing.ca

"It's not uncommon for the price of items to be hiked up a bit in order to offset the no-interest offer." - Lisa Rennie, Senior Contributor, Loans Canada

For example, some Canadian dealerships charge an $850 finance or lease fee that gets added to your total cost. It’s a good idea to compare the price of the vehicle under the 0% deal with what you might pay using traditional financing by navigating Canadian car dealerships with a clear strategy. If the dealer is unwilling to negotiate the price because of the financing offer, it could be a sign that the "savings" are already baked into an inflated sticker price.

How 0% Financing Works

0% financing is a promotional loan that allows you to repay only the principal amount borrowed - completely skipping interest charges. These deals are typically arranged through the automaker's own financing arms, like Toyota Financial Services, Honda Canada Finance, or Ford Motor Credit, rather than traditional banks or credit unions. This setup gives manufacturers more control over the terms and conditions, which is key to how these offers work.

Automakers Handle the Interest Costs

When you see a 0% financing offer, the automaker is actually covering the interest as part of their marketing strategy. This is known as an interest subsidy. It’s a way for manufacturers to make their vehicles more appealing, especially when they need to clear out older inventory or make space for new models. However, this "free" financing often comes with a catch: the sticker price vs MSRP might be higher, or you might have to forgo other incentives like cash rebates. Understanding how to use invoice pricing can help you determine if the 0% offer is truly the best deal. Essentially, the cost of the interest is shifted elsewhere, but every dollar you pay goes directly toward the principal.

Payments Go Directly to the Principal

With 0% financing, your monthly payments fully reduce the loan's principal. As Lisa Rennie, a Senior Contributor at Loans Canada, puts it:

"0% financing allows you to pay what an all-cash buyer would be paying, with the difference being that you can spread out the payments in installments over time."

For example, if you finance a $40,000 vehicle at 0% over 60 months, your monthly payment would be about $666.67. There are no added interest costs. Compare that to a traditional loan at 5% APR over the same term, which could add nearly $4,000 in interest. However, 0% financing often comes with shorter loan terms - commonly 24 to 36 months - resulting in higher monthly payments.

Pros and Cons at a Glance

Here’s a quick breakdown of the benefits and trade-offs of 0% financing:

| Aspect | Advantage | Disadvantage |

|---|---|---|

| Cost Savings | No interest charges over the loan term | Could mean a higher vehicle price or loss of other incentives |

| Accessibility | Payments are spread out without added interest | Requires excellent credit (typically 700–760+) |

| Flexibility | Simplified financing directly through the dealership | Limited to certain new models or trims |

| Repayment | Speeds up loan payoff | Higher monthly payments due to shorter terms |

It’s worth noting that 0% financing is almost always reserved for new vehicles. Used cars rarely qualify because manufacturers don’t have the same motivation to subsidize older inventory. Additionally, these offers are typically available only to borrowers with excellent credit scores, making them less accessible to those with lower credit ratings.

How to Evaluate and Apply for 0% Financing

0% Financing vs Traditional Loan: Cost Comparison Calculator

Taking advantage of a 0% financing deal can be a smart move, but it’s important to evaluate these offers carefully to ensure they’re truly worth it.

Research Current 0% Financing Promotions

As of February 2026, several Canadian manufacturers have enticing 0% financing deals. For example, the 2026 Ram 1500 Laramie and the 2026 Buick Envision both offer 0% financing for 60 months. The 2026 Chrysler Pacifica Select AWD goes even further, providing 0% financing for up to 72 months, while the 2025 Volkswagen ID.4 also offers 0% for 60 months. These promotions are typically limited to specific models and trims, and they’re offered through the manufacturer’s financing arm. To confirm availability in your province, check the manufacturer’s website or visit a local dealership.

Check Your Credit Score

Before applying, ensure your credit score meets the lender’s requirements - usually 725 or higher. You can access your credit report through Equifax or TransUnion to verify your score and address any potential issues. Having a strong credit profile is critical since 66% of Canadians prefer financing directly through dealerships for convenience.

Negotiate the Vehicle Price Separately

Once you’ve confirmed your eligibility for 0% financing, focus on negotiating the vehicle’s price. Dealers might be less flexible on the sticker price when offering 0% financing, as they’re covering the interest cost themselves. Stephanie Wallcraft, a freelance writer for Driving.ca, suggests:

"Simply state firmly that you're not interested in discussing financing or trade-in terms until the cost of the car is settled."

To gain an advantage, research the dealer invoice price - the amount the dealer pays the manufacturer. Tools like Unhaggle or Car Cost Canada can provide this information. Start negotiations slightly above the invoice price (1% to 5% higher) instead of working down from the MSRP.

Compare Total Costs Using Invoice Pricing Tools

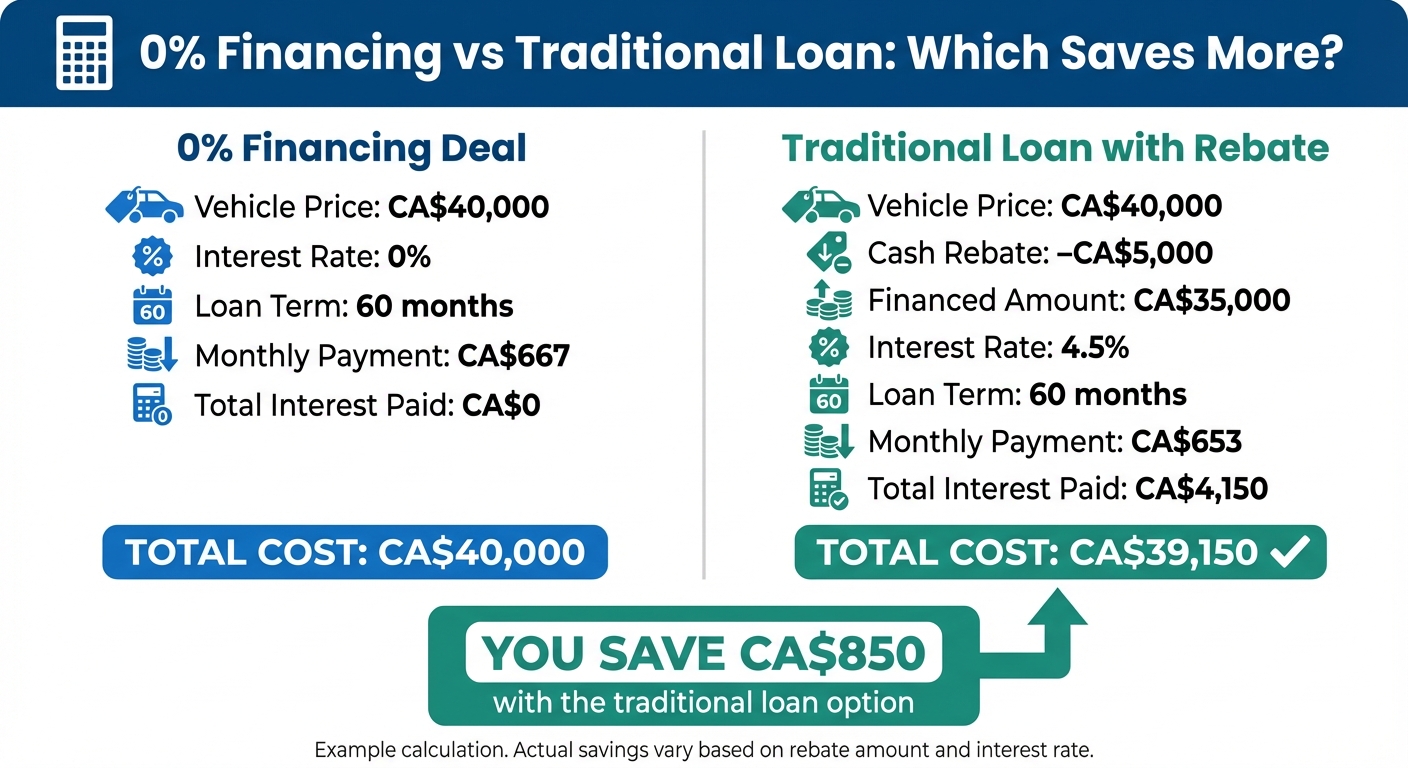

It’s essential to calculate whether the 0% offer saves you money in the long run. Transparent pricing tools can help you compare dealer prices and MSRP. For instance, if you finance CA$40,000 at 0% over 60 months, your total cost will remain CA$40,000. However, if you’re offered a CA$5,000 cash rebate with a traditional loan at 4.5% interest over the same term, you’d finance CA$35,000 instead. In this scenario, your total repayment would be about CA$39,150, saving you roughly CA$850.

By comparing these costs, you can determine whether the 0% financing deal or a cash rebate with a standard loan offers better value.

Compare with Other Financing Options

Many 0% financing promotions require you to choose between the interest-free loan and a cash rebate - you typically can’t have both. OnPath Credit Union highlights the exclusivity of these deals:

"Dealers use it as bait to get folks in the door, but only the most creditworthy borrowers walk away with the deal."

To make an informed decision, consider getting pre-approved for a loan from your bank or credit union to establish a baseline interest rate. Then, compare the total costs of the 0% financing deal against a traditional loan that includes a cash rebate. Keep in mind that 0% offers often come with shorter terms (24 to 48 months), resulting in higher monthly payments. If you need more flexibility, a longer-term loan at a low interest rate might be a better fit for your budget, even if it costs slightly more overall.

Conclusion

Zero per cent financing can be appealing to Canadian car buyers, but it’s not a universal solution. These offers typically require excellent credit (usually a score of 725 or higher) and often come with trade-offs, such as choosing between 0% interest and cash rebates or shorter loan terms that lead to higher monthly payments. While the idea of paying no interest sounds attractive, the benefits can be diminished by higher vehicle prices or lost rebates.

A smart approach is to negotiate the vehicle price first, before diving into financing discussions. Take the time to crunch the numbers - compare the total cost of a 0% financing deal to that of a standard loan with a cash rebate. Depending on the rebate size and the interest rate, the standard financing option might actually save you more money.

Tools like Price Driven can provide valuable insights into dealer pricing and help you determine if a 0% financing offer is truly competitive. Their free discount reports reveal invoice-level pricing, while their $99 pre-negotiated pricing service guarantees savings with partner dealerships across Canada.

It’s worth noting that 93% of Canadians focus on monthly payment amounts rather than the annual percentage rate (APR). However, concentrating solely on the monthly payment can lead to paying more over the loan term. To avoid this, consider getting pre-approved for financing through your bank or credit union before heading to the dealership. Also, be sure to read the fine print carefully for details like deferred interest or restrictions on combining offers.

Ultimately, 0% financing is best suited for buyers with strong credit who can handle higher monthly payments and ensure the vehicle price isn’t inflated. For others, a low-interest loan combined with a cash rebate might deliver greater savings.

FAQs

Will 0% financing raise my total vehicle price?

When you see a 0% financing offer, it might seem like a great deal at first glance. However, manufacturers often tweak the vehicle's pricing to make up for the interest-free loan. For instance, they might remove discounts or slightly raise the base price. This means that even without paying interest, you could still end up spending more overall.

Is 0% financing better than a cash rebate plus a low APR?

0% financing might sound like a great deal since it eliminates interest charges, but its actual value depends on the fine print. Sometimes, these offers come with hidden costs or restrictions. For example, the price of the vehicle might be higher, or you could miss out on other discounts. In some cases, choosing a cash rebate combined with a low-interest loan could save you more in the long run - especially if you qualify for a competitive rate through another lender. To figure out which option suits you best, compare the total costs, keeping your credit score and potential savings in mind.

What fees or fine print can cancel out a 0% deal?

Hidden fees, inflated vehicle prices, steep interest on overdue payments, and the risk of losing rebates or discounts can quickly outweigh the perks of a 0% financing offer. These issues can drive up the overall cost, sometimes making it pricier than a regular loan. Be sure to carefully examine the terms to confirm that the deal actually delivers the savings it promises.